Generative AI is no longer a novelty in financial services. As of early 2026, regulators treat it as a supervised technology that demands the same compliance rigor as any critical system. The Financial Industry Regulatory Authority (FINRA) made this clear in its December 2025 Annual Regulatory Oversight Report, marking a pivotal shift from viewing AI as an emerging trend to enforcing strict oversight. For banks, insurers, and investment firms, this means traditional Model Risk Management (MRM) practices are insufficient on their own. You need a new approach that addresses the probabilistic nature of generative models, their data dependencies, and the real risk of discriminatory outcomes in lending.

Key Takeaways

- Regulatory Shift: FINRA and the SEC now require dedicated AI governance programs integrated with existing MRM frameworks.

- Compliance-Grade AI: Systems must achieve 95%+ output consistency and maintain 100% audit trails for all decisions.

- Fair Lending Focus: Unmonitored AI models face severe penalties; CFPB recently fined a lender $12.7 million for AI-driven bias.

- Implementation Cost: Expect $2.3 million average setup costs and 6-9 month deployment timelines for major institutions.

- Human-in-the-Loop: Mandatory human validation is required for all customer-facing outputs and decision-influencing applications.

The New Regulatory Landscape for GenAI

The rules have changed. In November 2025, the Securities and Exchange Commission (SEC) withdrew its proposed rule on predictive analytics, signaling a preference for technology-neutral principles rather than AI-specific bans. This doesn't mean leniency. SEC Chair Gary Gensler stated clearly at MIT in late 2025 that existing rules on fair lending, market manipulation, and investor protection apply with full force to AI systems. The focus has shifted to how you govern these tools, not whether you can use them.

By January 2026, 78% of major financial institutions had established dedicated AI governance committees. This surge reflects a broader industry recognition that Generative AI introduces unique risks like hallucination, bias propagation, and lack of determinism that standard IT controls miss. If you're still treating your AI prompts like casual email drafts, you're already behind. Regulators expect prompt logging retained for a minimum of seven years under SEC Rule 17a-4, alongside version tracking for every model iteration.

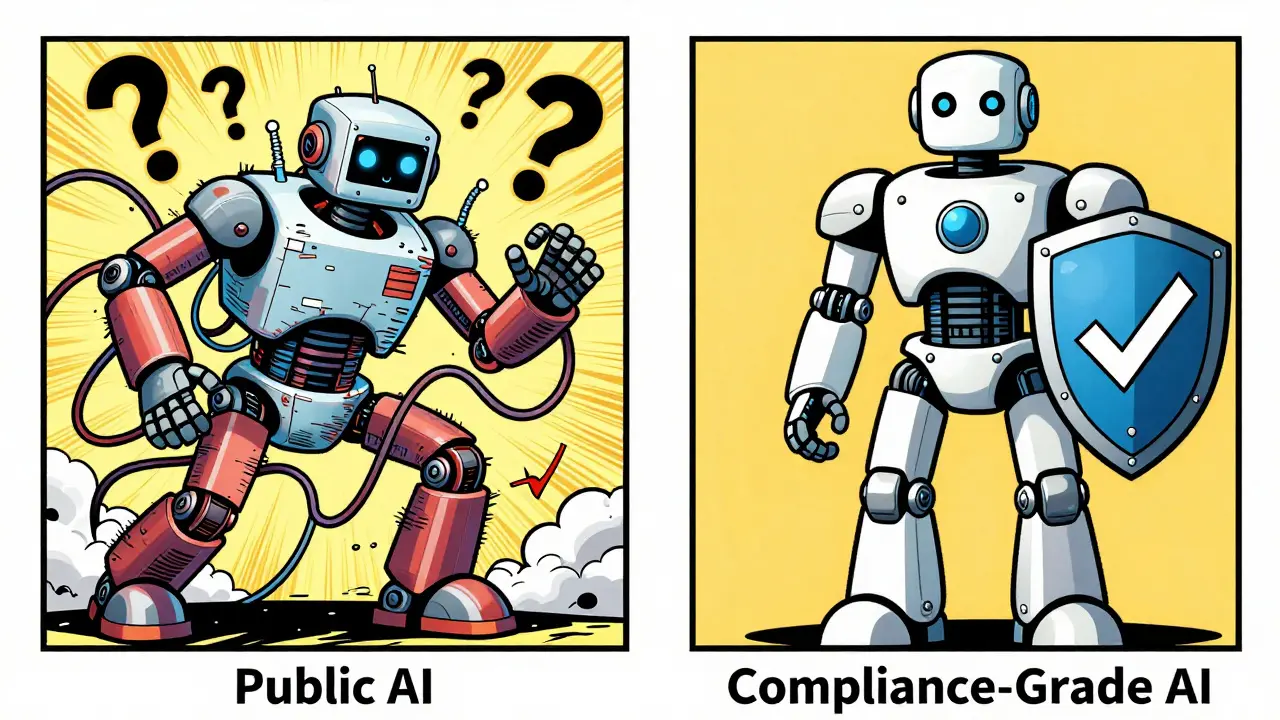

What Is Compliance-Grade AI?

You can't just plug public ChatGPT into your loan approval workflow. Red Oak Analytics defines "Compliance-Grade AI" as an architectural approach with three non-negotiable pillars:

- Determinism: Outputs must be consistent, achieving 95%+ accuracy for identical inputs.

- Full Traceability: A 100% audit trail of data lineage and decision pathways is mandatory.

- Constrained Action Spaces: AI outputs are limited to pre-approved parameters only.

This differs sharply from conventional generative AI. FINRA testing revealed that public tools like ChatGPT showed a 37% error rate in interpreting financial regulations. In contrast, enterprise-grade compliance systems leveraging decades of real-world data achieved 92% accuracy. The trade-off? Compliant systems typically run 15-25% slower due to safety checks. However, leading institutions report 40-60% reductions in document processing times overall because the errors-and subsequent rework-are eliminated.

Fair Lending and the Bias Trap

Fair lending is where the stakes are highest. The Consumer Financial Protection Bureau (CFPB) announced its first enforcement action related to AI-driven lending discrimination in January 2026, fining a major online lender $12.7 million for violating Regulation B through unmonitored model drift. This case serves as a stark warning: if your AI inadvertently uses prohibited demographic factors, you are liable.

Compliance-grade systems demonstrate 98.7% consistency in loan approval criteria across demographic groups, compared to just 82.3% in non-compliant setups. To achieve this, you must implement bias testing protocols specifically for generative AI. FINRA’s January 2026 guidance requires quarterly testing for high-impact lending applications by June 30, 2026. Without proper monitoring, 31% of tested AI lending models showed significant bias deterioration within 90 days of deployment, according to CFPB data from late 2025.

Implementing Human-in-the-Loop Controls

Automation without oversight is a compliance nightmare. Every customer-facing output or decision-influencing application requires documented sign-offs from designated supervisory owners. This is known as Human-in-the-Loop validation.

In practice, this means adding checkpoints. Keyrus’s 2026 survey found institutions average 7.2 validation points per workflow. While this increases response times by roughly 22%, it prevents catastrophic errors. One compliance officer on Reddit reported that their prompt logging system caught 147 instances where the AI would have violated Reg B-saving them millions in potential penalties. The key is training staff effectively; top firms provide 40+ hours of AI literacy training to compliance teams annually.

The VALID Framework for Daily Operations

To manage day-to-day risks, many experts recommend the VALID framework. It provides a practical checklist for employees using generative AI:

- Validate: Never trust AI output blindly; verify against source documents.

- Avoid personal information: Never input sensitive client data into public models.

- Limit scope: Use AI only for pre-approved use cases.

- Insist on transparency: Document which model was used and why.

- Document everything: Keep logs of prompts and responses for audits.

This framework helps bridge the gap between technical capabilities and regulatory requirements. It ensures that even if the model behaves unpredictably, the institution maintains control over the process.

Costs, Timelines, and Market Reality

Building compliant infrastructure isn't cheap. FTI Consulting estimates the average implementation cost at $2.3 million per major institution. Deployment takes 6-9 months, broken down into three phases:

- Phase 1 (30-45 days): Establish AI governance with clear ownership across business, compliance, tech, and risk functions.

- Phase 2 (60-90 days): Pre-approve use cases with written purpose statements and data source documentation. Note that 63% of institutions face delays here due to poor vendor documentation.

- Phase 3 (90-120 days): Build human-in-the-loop protocols and train staff. This is often the most resource-intensive phase.

Despite the upfront costs, Baker Donelson’s 2026 forecast suggests a 65% reduction in regulatory penalty risks for firms that invest properly. The regtech market targeting AI compliance has grown to $4.7 billion in 2026, reflecting this urgent demand.

Comparison: Public vs. Compliance-Grade AI

| Feature | Public Generative AI (e.g., ChatGPT) | Compliance-Grade AI |

|---|---|---|

| Regulatory Accuracy | 63% (High Error Rate) | 92% (Verified) |

| Output Consistency | Variable (Probabilistic) | 95%+ (Deterministic) |

| Audit Trail | None/Limited | 100% Traceable |

| Fair Lending Consistency | 82.3% | 98.7% |

| Implementation Cost | Low (Subscription) | High ($2.3M avg.) |

| Human Validation | Optional | Mandatory |

Future Outlook: What Comes Next?

The regulatory bar will only rise. FINRA expects to release guidance on "AI agent" accountability in Q3 2026, requiring explicit human responsibility for all AI-initiated actions. Meanwhile, the FCA’s Supercharged Sandbox Ecosystem is expanding to include cross-border validation, allowing UK and US firms to test frameworks jointly. By August 2026, companies will likely need to comply with specific transparency rules for high-risk AI systems as state-level regulations converge. The message is clear: adapt now, or face enforcement later.

What is the biggest risk of using generative AI in lending?

The biggest risk is unintentional bias leading to fair lending violations. If an AI model drifts and starts discriminating against protected classes, the institution faces massive fines, such as the recent $12.7 million CFPB penalty. Regular bias testing and human oversight are essential to mitigate this.

Do I need a dedicated AI governance committee?

Yes, especially if you are a major financial institution. As of early 2026, 78% of large firms have established these committees. They ensure that AI usage aligns with regulatory requirements like FINRA's 2026 guidelines and help manage model risk effectively.

How long does it take to implement compliant AI systems?

Expect a 6-9 month timeline. This includes establishing governance (30-45 days), approving use cases (60-90 days), and building human-in-the-loop validation protocols (90-120 days). Delays often occur due to insufficient vendor documentation.

What is the VALID framework?

VALID stands for Validate, Avoid personal information, Limit scope, Insist on transparency, and Document everything. It is a practical checklist for employees to ensure safe and compliant use of generative AI tools in daily operations.

Is public ChatGPT safe for financial analysis?

No. Public models lack the determinism, audit trails, and security controls required by regulators. FINRA tests showed a 37% error rate in regulatory interpretation for public tools. Always use enterprise-grade, compliance-certified AI systems for professional tasks.

What happens if my AI model drifts?

Model drift can lead to biased outcomes and regulatory penalties. The CFPB reports that 31% of unmonitored AI lending models show significant bias deterioration within 90 days. You must implement quarterly bias testing for high-impact applications to catch and correct drift early.